Newly released data sheds light on the $38.5 billion in federal coronavirus assistance New York businesses received to keep small businesses afloat and keep workers on payroll.

At least 323,900 loans were issued to New York businesses.

In a statement on Monday, the federal government's Small Business Administration rep Jovita Carranza said the numbers show "small businesses of all types and across all industries benefited from this unprecedented program."

But some disparities remained—with high-paying industries getting more loan dollars per job and typically-flourishing business centers getting some of the least amount of loans.

For instance, in New York City, a RentHop report found Flushing, Bay Ridge, the Upper East Side, Corona, and Bath Beach had the fewest percentage of PPP loans compared to the number of qualified businesses, according to census data.

Some 913 PPP loans were approved out of 2,381 businesses in Flushing—a 38.3 percent rating.

Meanwhile, Greenpoint, Park Slope, Brooklyn Heights, the Financial District, and Carnegie Hill saw the highest percentages of loans out of qualified businesses—ranging from 70 to 78 percent.

The executive director of the Greater Flushing Chamber of Commerce, John Choe, found the data point concerning.

Though small business owners he's spoken to have seen the efficiencies in the PPP system improve over time, "the fact that our businesses were not being served by the federal government is really distressing," Choe said.

"We're not a small out of the way neighborhood," Choe added. "If there's a program that's supposed to be helping small businesses, you go to the neighborhoods with one of the highest concentration of small business, and yet it doesn't seem like that outreach effort of trying to support small businesses and the small business hub of New York took place."

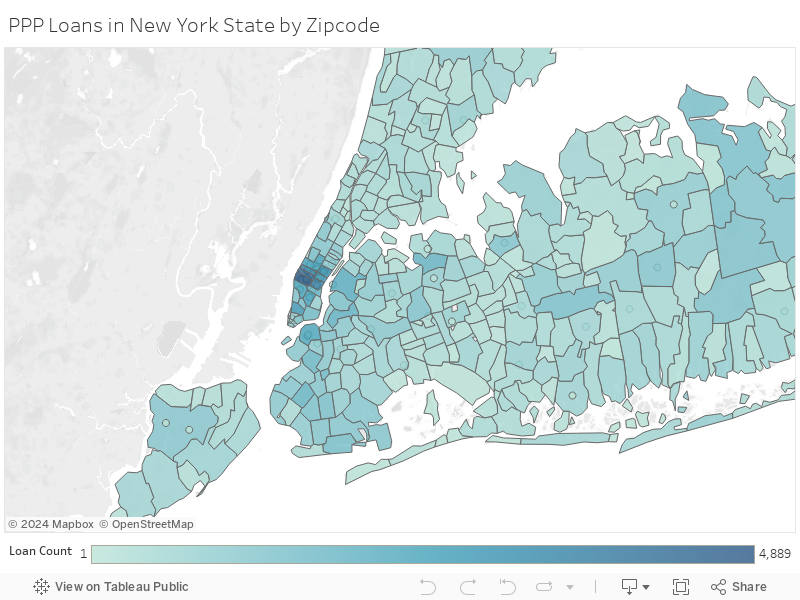

Here's a map of where PPP loans, both large and small, were approved:

Here's PPP loans in New York State by amount:

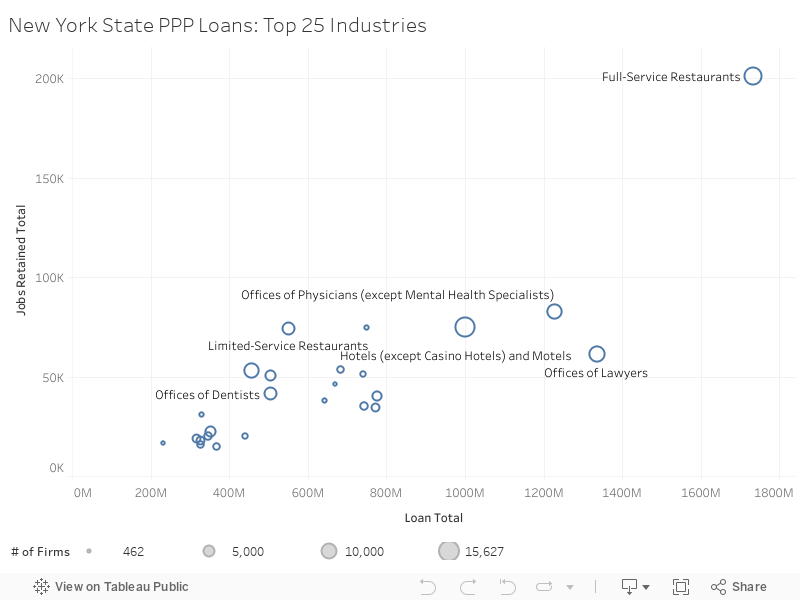

Here's which industries benefited the most:

Here's the top 25 industries by loan dollar amount per job retained, which was calculated using the midpoint of loan averages, since only loan ranges were provided, not the exact dollar amount:

The SBA's dataset is an early picture of how the federal forgivable PPP loans operated across the country, showing which loans were approved, according to the information lenders provided to the SBA.

Some businesses are listed in the data but ultimately didn't take a loan, like electric scooter company Bird or and investment firm Index Ventures. To be removed from future reports, a business would have to request its lender to cancel the loan in the SBA system, according to an administration spokesperson.

The dataset shows that 5,800 large loans claimed to save zero jobs—though the data may have inaccuracies or not be up-to-date. About 50 companies that got $5 to $10 million show zero jobs retained at all.

Scores of businesses showed just one or a handful of jobs retained. (According to the SBA data, New York Public Radio, the non-profit parent company of WNYC and Gothamist, received a "$5-10 million" loan from the PPP program, through Boston Private Bank & Trust Company. The filing indicated NYPR would retain 467 jobs.)

Dozens of businesses Gothamist/WNYC contacted that reporteed little to no job retainment in the SBA's dataset either declined comment, hung up the phone, said they'd get back to us or to call back another time, did not respond to an inquiry, or had incorrect contact information listed.

One business's representative, a Marriott hotel called W South Beach, with a company address in Manhattan, said the dataset was inaccurate, and that it had paid all its hotel employees for the two-month PPP period, but declined to comment further. It was approved for $2 to $5 million, but the dataset says it only retained two jobs.

"It actually may be too early to really evaluate these numbers because I think what's going to be more critical is what the companies report at the time when they're seeking forgiveness for these loans," said Phil Mattera, the research director at Good Jobs First. "So the question will be, what do they report later, and how careful are they?"

Business leaders on the ground saw a shift in how accessible the PPP loans were for small businesses between the first and second round of federal stimulus money.

"In terms of access, the data shows the PPP program was a success for most businesses," Randy Peers, the president of the Brooklyn Chamber of Commerce said in an email.

The second round had community development financial institutions participate, and larger banks and publicly traded companies, like Shake Shack, heard loud and clear the backlash about small businesses getting shortchanged. (While Shake Shack's Danny Meyer declined money for his burger chain, he ended up taking more than $10 million for his other businesses.)

"Getting a loan, having it forgiven, and using it effectively are three different issues, however, and not all businesses that received a loan are in the same boat," Peers added. "When you applied and received the funds, and when your business could actually open, are the critical variables that determine if this program really helped a business survive long-term."

Other highlights:

- 46,888 loans above $150,000 were issued, and 277,012 loans below $150,000 were issued.

- For large loans, restaurants got $1.3 billion, saving 109,000 jobs. Lawyers were approved for another billion, saving 42,000 jobs. Physicians and home health care services saw 54,000 and 71,000 jobs saved, respectively.

- The top five industries for small loans included restaurants, lawyers, international affairs, physicians and real estate agents.

- Industries that already paid better wages were approved for more loan dollars for every job saved. For instance, the program paid out $24,000 per job for lawyers and $10,000 a job for home health care services, according to the large loan dataset.

- The biggest lender for large loans was JPMorgan Chase Bank with 9,263 approved loans. More than half were for $150,000 to $350,000 loans. The next top lenders were Manufacturers and Traders Trust Company, TD Bank, Bank of America, KeyBank, and Citibank.

- For loans less than $150,000, the top five lenders were JP Morgan Chase Bank—49,423 loans for an average of $39,460—and then TD Bank, Bank of America, Kabbage, Inc., Cross River Bank, and Celtic Bank Corporation.

- The top five zipcodes for loan approval were in Midtown for both small and large loans. More than 900 zipcodes statewide had 20 or fewer loans for both categories.

- Not many conclusions can be drawn on whether minority- and women-owned businesses received a fair share. About 80 percent of applicants left gender unanswered, and 93 percent of race and ethnicity data was unavailable.

- Some addresses showed up repeatedly. Nine addresses alone had more than 10 loans registered, indicated some businesses may have gotten approval for loans through a loophole allowing each location of a business—like a restaurant—to get a loan if it has less than 500 employees.